")

The FIRE movement has been rattling around in my head for years now, like, seriously, ever since I stumbled on some blog back in my late 20s and thought, “Wait, financial independence retire early sounds freaking amazing.” I’m sitting here in my cozy but kinda cramped apartment in the Midwest—it’s December 2025, snow’s piling up outside my window, and the heater’s cranking because, yeah, utility bills are no joke these days. Anyway, I’ve been chasing this FIRE thing on and off, saving like a maniac some months, then totally blowing it on takeout when life gets overwhelming. And honestly? In 2025, with everything costing an arm and a leg, I’m wondering if the FIRE movement is still legit or if it’s just some outdated dream from lower-inflation times.

whatastupidnameforawebsite.com

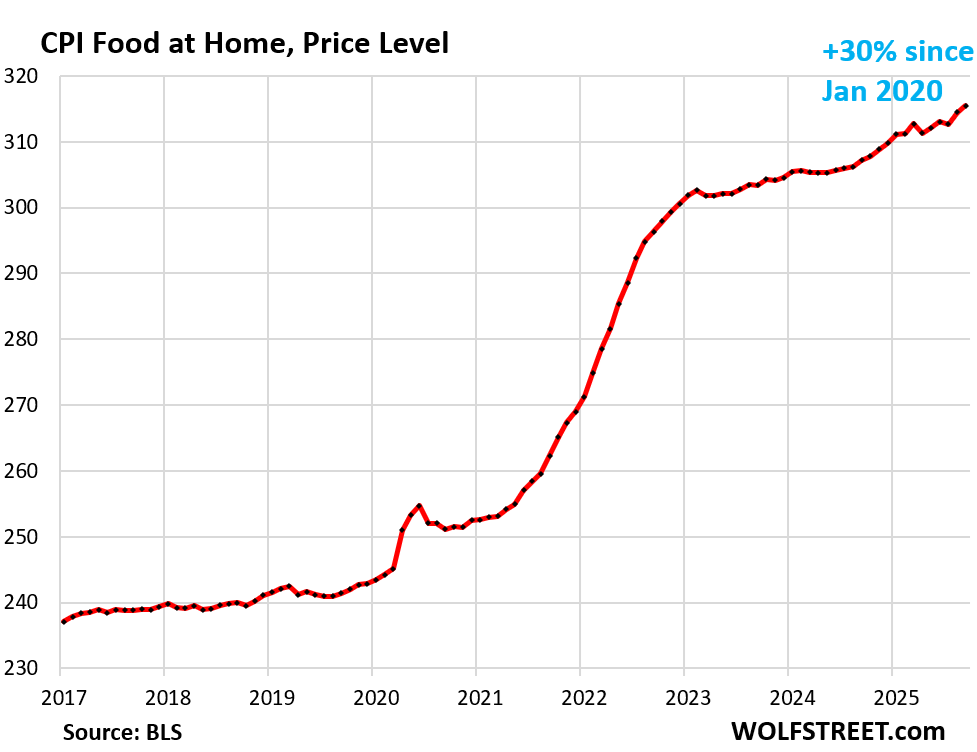

I gotta be real with you—my own journey into the FIRE movement started messy. Back in 2020, I was drowning in student loans, living paycheck to paycheck in a tiny rental, eating ramen like it was gourmet. Then the pandemic hit, and I got laid off for a bit. Scary as hell, but it forced me to side hustle like crazy—driving for Uber Eats, freelancing on the side—and I started dumping every extra dollar into index funds. Felt empowering, you know? But fast forward to now, and inflation’s cooled to around 2.7%, but prices are still sky-high from those wild years. Groceries? Forget it. I remember blushing hard at the checkout last week when my “frugal” cart hit $150 for basics. Embarrassing, but yeah, that’s the raw truth of trying financial independence retire early in this economy.

Why the FIRE Movement Feels Tougher in 2025

Look, no sugarcoating—the challenges to the FIRE movement in 2025 are real, y’all. Housing prices are insane; median home’s around $410,000 or something ridiculous like that, and rents? In my area, a decent one-bedroom is pushing $1,500 easy. I almost bought a place last year, crunched the numbers, and nope—mortgage would’ve eaten half my take-home. Seriously, how do you save 50-70% of your income for financial independence retire early when basics suck up so much?

And healthcare? Don’t get me started. Pre-Medicare, premiums are brutal if you’re retiring early. I had a scare last year with some random ER visit—bill was thousands even with insurance. Made me rethink the whole 4% rule thing. Stocks have been killer, S&P up big again this year, but volatility? One bad dip and your FIRE plans feel shaky. I’ve had nights staring at my portfolio, heart pounding, thinking, “Is this financial independence retire early dream just gonna crash?”

My Personal Flubs and Wins Chasing FIRE Movement Goals

Okay, confession time—I’ve screwed up plenty trying this FIRE movement stuff. There was that phase where I went ultra-frugal, like, no eating out, no fun, and I burned out hard. Ended up binge-spending on a vacation I couldn’t afford, felt guilty for months. Self-deprecating much? Yeah, that’s me. But wins too: Started a side hustle blogging about personal finance (ironic, right?), and it’s brought in extra cash to throw at investments. Maxed my 401(k) this year—limits are up to $23,500, thank god—and Roth IRA too.

Here’s some stuff that’s worked for me, flawed as I am:

- Track everything, obsessively: I use a janky spreadsheet—nothing fancy—but it keeps me honest on spending.

- Side hustles saved me: Freelance gigs, even dumb ones like surveys sometimes, add up for that aggressive saving vibe central to the FIRE movement.

- Invest simple: Mostly broad index funds. No day trading nonsense after I lost money trying to be clever early on.

- Geo-arbitrage daydreams: Thinking of moving somewhere cheaper, like the South, to stretch dollars further toward financial independence retire early.

But contradictions? Totally. I preach frugality but love good coffee. Sue me—I’m human.

Is the FIRE Movement Still Possible in 2025? My Take

Yeah, it is—but it’s evolved, man. Not the extreme “retire at 30 on rice and beans” anymore for most. More like flexible financial independence, maybe Barista FIRE with part-time work for health insurance. Sources like JL Collins still swear by the simple path, and with markets performing solid, it’s doable if you’re disciplined. But for average folks? Harder with costs up. My portfolio’s growing, but slowly—feels bittersweet.

Anyway, wrapping this ramble: The FIRE movement isn’t dead in 2025; it’s just realer, with more hurdles. If you’re chasing financial independence retire early, start small—track spending today, bump savings tomorrow. Talk to a financial advisor, read up (check out Mr. Money Mustache or ChooseFI for inspo). What’s your story? Drop a comment if you’re on this path too. Let’s chat—might make my own journey less lonely.

(References: For more on current trends, see Ironwood Wealth Management on FIRE in 2025, Investopedia’s FIRE guide, and BLS inflation data.)

{kind=link}